India’s auto sector closed September 2025 on a mixed note. GST 2.0 tax reforms and festive sentiment lifted market mood, but retail registrations dipped ~13% YoY as buyers delayed purchases until post-GST revision. Exports played a crucial role in cushioning OEM volumes.

Passenger Vehicles: SUVs & EVs Lead the Charge

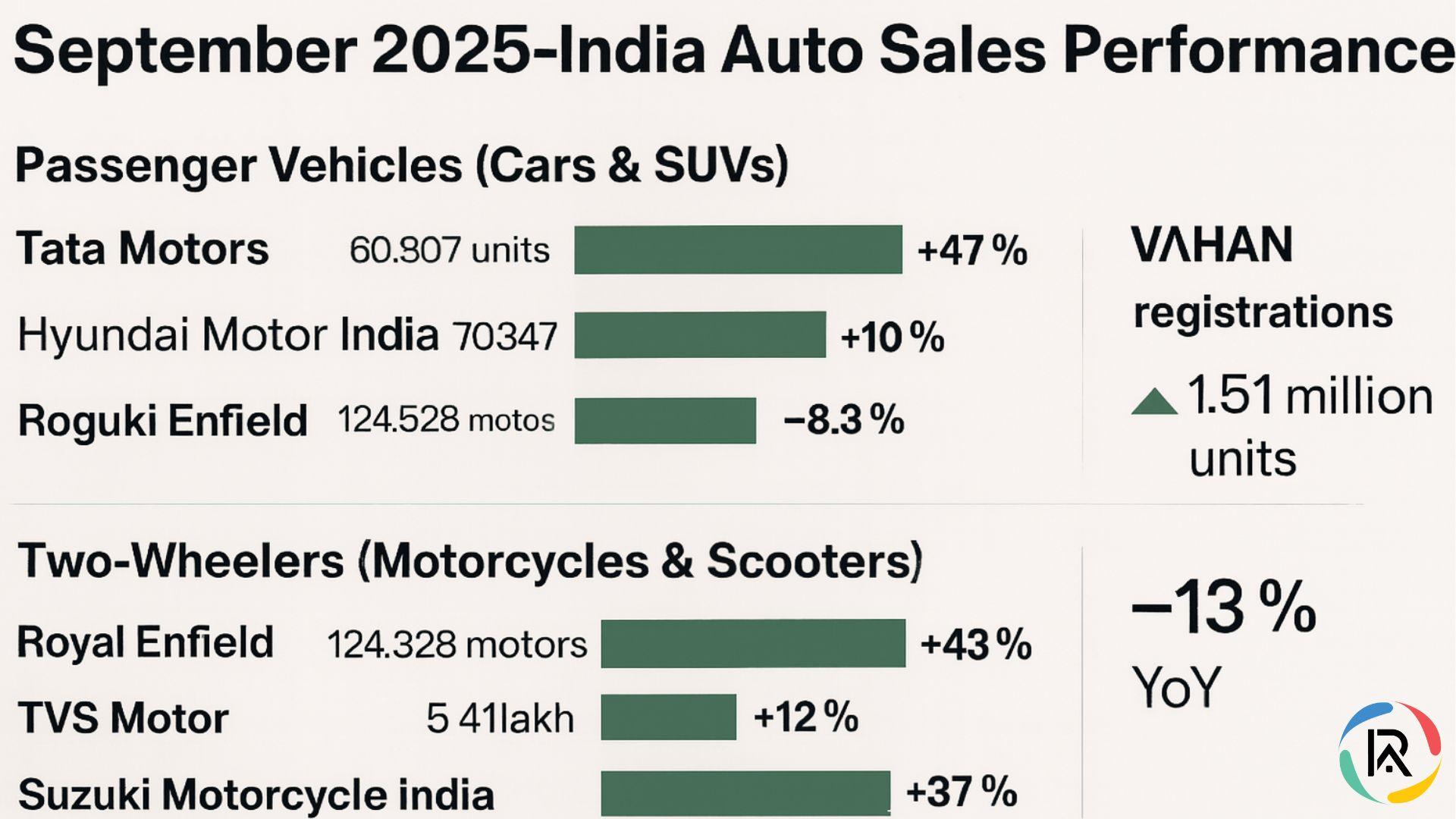

- Tata Motors posted its highest-ever monthly sales, delivering 60,907 units (+47% YoY). Strong SUV momentum and rising EV penetration consolidated its leadership position.

- Hyundai Motor India reported 70,347 units (+10% YoY), aided by exports that touched a 33-month high.

- Mahindra & Mahindra grew SUV volumes by ~10% YoY, benefitting from rationalised GST slabs on larger SUVs.

- Maruti Suzuki sold 1,89,665 units. Domestic sales fell (−8.3% YoY) to 1,35,711 units, but exports surged 52%, cushioning overall volumes.

Two-Wheelers: Premium Motorcycles & Scooters Outperform

- Royal Enfield recorded its best-ever monthly sales at 1,24,328 motorcycles (+43% YoY), underscoring strong demand in the mid-size segment.

- TVS Motor Company sold 5.41 lakh units (+12% YoY). Scooter sales (+17%) outpaced motorcycles (+9%), while its EV portfolio advanced steadily (+8%).

- Suzuki Motorcycle India achieved 37% growth in domestic sales, led by Access and Burgman scooters.

- Bajaj Auto registered 9% YoY growth in two-wheeler sales, driven largely by exports of Pulsar and Dominar models.

Key Market Drivers in September 2025

- GST 2.0: Small car GST cut to 18%, SUV cess eased

- Festive demand: Navratri spurred sales, Diwali expected stronger

- Exports: Shielded OEMs from domestic softness

- Premiumisation: Rising preference for SUVs & mid-size bikes

Outlook:

Q3 FY2025–26 looks stronger with festive tailwinds, GST relief, and robust exports. Financing challenges and short-term retail weakness remain watchpoints.